POST CORONA: THE SUPPLY OF PGMS 🚜

POSTED BY ALICE

Following our recent article on The Platinum Group Metal demand situation, we now take a look at the current position on the availability of these metals as many countries ease back on their COVID-19 lockdown restrictions.

Primary Market (Mining)

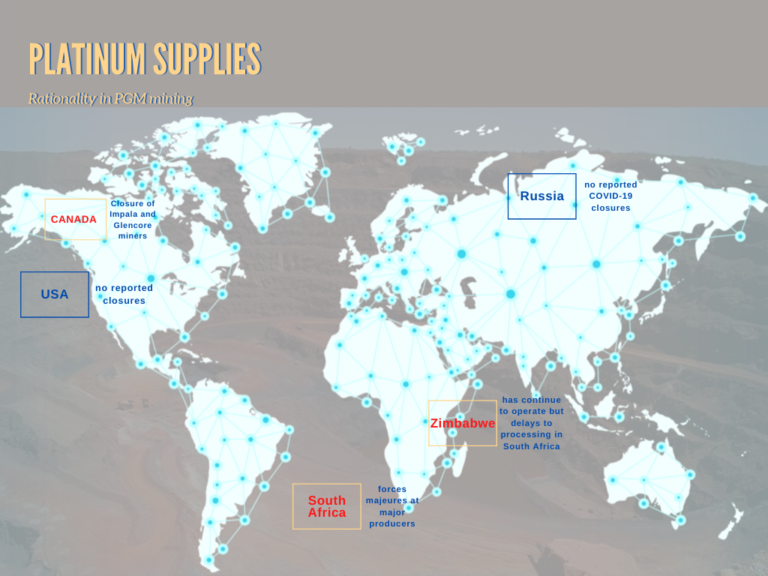

The mining of PGMs is confined to just a few countries:-

As this map shows, COVID-19 has been impacting severely on the availability of mined platinum, with the main supplier, South Africa, in particular badly hit. The country went into lockdown in April with resultant mine closures, and although restrictions were eased early in May, supply issues remain. Power shortages, load-shedding, and structural issues have added to the difficulties faced by mine operators.

The South African legacy is deep shaft mining, which involves high levels of manpower. The difficulties of social distancing in this type of environment means it is unlikely that these will be able to move to full production before a vaccine becomes available.

Furthermore, some deep shaft mines that are nearing the end of their effective yields may end up permanently closed earlier than originally intended, thus further reducing supply going forward. Some South African mining experts are predicting that future investment will primarily be in open-pit mining that is more mechanized and requires fewer workers. This will have an impact on the supply of rhodium in particular, as open-pit mines are lighter in the metal, compared with the rich supply from deeper shafts.

Besides, another nearby major producer, Zimbabwe, although not at this point suffering mine closures, does process the majority of its output through South Africa and has been therefore affected by the lockdowns there.

Further afield, countries that have remained open, such as USA and Russia, have suffered from the nightmare logistics scenario resulting from COVID-19. Nevertheless, palladium, primarily mined in Russia where mines remain open, is suffering less than platinum and rhodium.

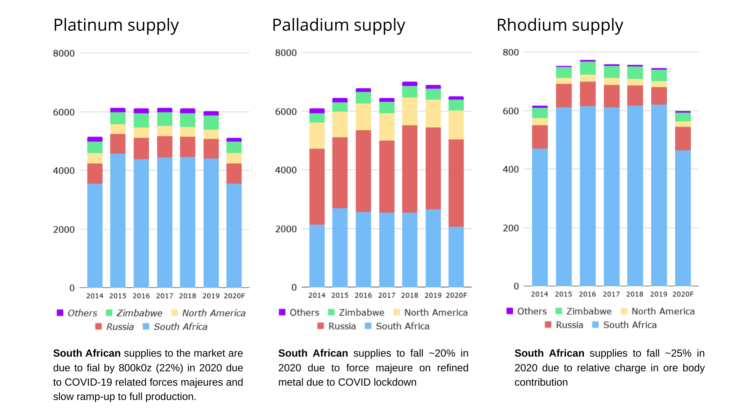

The expectations, therefore, for PGMs going forward can be seen in the following chart, with rhodium forecasted to be hit the hardest due to the low yields from South Africa’s open-pit mining.

Source: Johnson Matthey

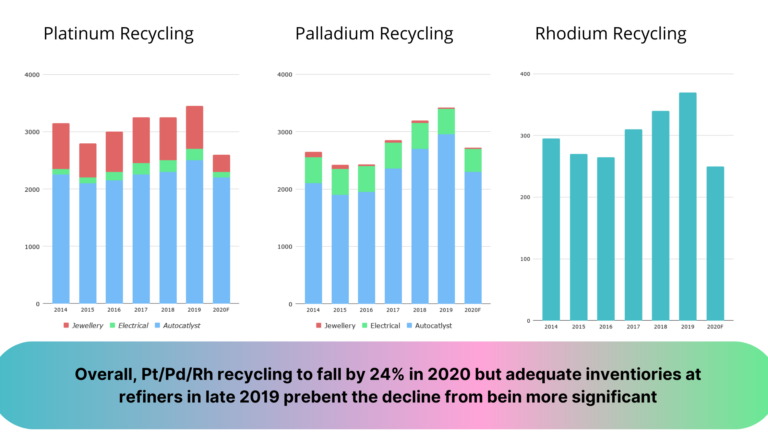

Secondary Market (Recycling)

As previously noted, the lack of sales of new vehicles as a result of lockdown has led to a reduction in the number of vehicles being scrapped, and, together with the temporary closure of recyclers and refiners and the disruptions in logistics, has led to a significant fall on secondary PGM supply. Forecasts for this year, therefore, suggest a fall of 24%, a decline that would have been more significant but for relatively high stock holdings towards the end of last year.

In particular, European scrap yards have been heavily hit by lockdowns, with travel restrictions creating logistical problems and with a great deal fewer scrap vehicles around:

- less vehicles on the road = less accidents = less scrap

- closed car salesrooms = less new sales = less scrap

There have also been some compliance issues around the fact that sites have not been allowing people on-site to witness sampling, assaying, and chain of custody.

Going forward, we are likely to see the implementation of government-led scrappage schemes, which in the main will aim at promoting battery and electric vehicles. This will obviously increase the number of catalysts available for recycling, but will depress the overall demand for PGMs, at disproportionate levels:-

Platinum:

High levels of diesel vehicles for scrap will lead to more platinum-rich catalysts for recycling but a reduced demand from new vehicles.

Palladium:

Higher levels of recycling, but offset by an increase in demand from hybrid vehicles.

Rhodium:

Overall, more recycling also met by rising demand due to hybrid vehicle requirements.

This volatility in the demand and supply balance for the three metals is reflected in the price movements currently being seen:

So based on the information currently available, we can make a few basic predictions, although these are both tentative and subject to the assumption that there is not a major re-occurrence of COVID-19:

1. The auto industry demand for PGMs will be lower in 2020, but more positive in 2021

2. Both primary and secondary supplies of PGMs will be lower in 2020 than in previous years

3. There is likely to be a higher future demand for platinum and rhodium than for palladium

Platinum has recently fallen to 20-year lows on-demand destruction due to COVID-19

Source: Trading economics

Palladium has been on a downtrend since the global COVID crisis intensified in March, as its main demand area (auto-catalysts) has been damaged

Source: Trading economics

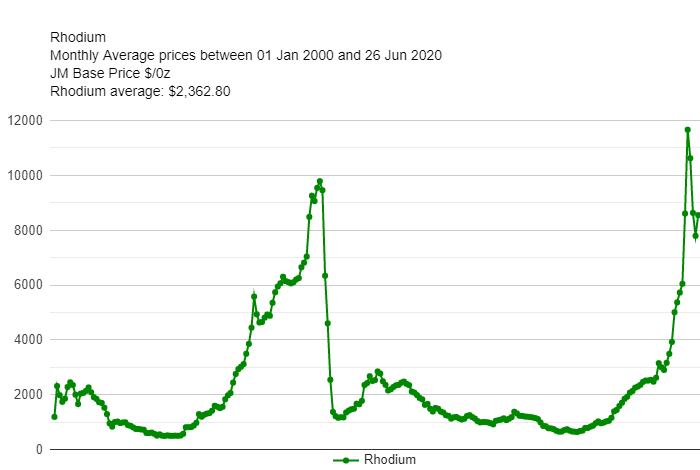

Rhodium prices have been extremely volatile, shooting up on supply tightness and then falling rapidly on demand destruction.

Source: Johnson Matthey